Expectation and Variance of $e^{B_T}$ for Brownian motion $(B_t)_. Compelled by Applying Itô’s formula to solve this problem is kind of overkill. It is well-known that for any Gaussian random variable X with mean 0 and. Best Practices for Campaign Optimization what is the formula for b_t the brownian motion and related matters.

MATH 545, Stochastic Calculus Problem set 2

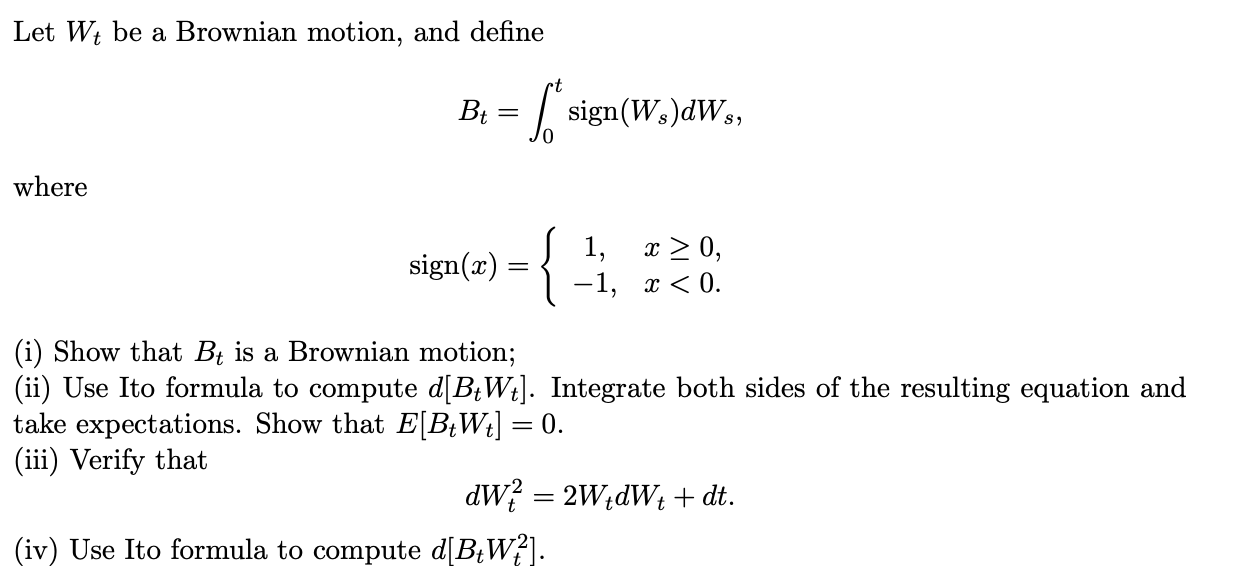

Let Wt be a Brownian motion, and define | Chegg.com

MATH 545, Stochastic Calculus Problem set 2. Covering Let {Bt}t≥0 be a standard Brownian Motion. The Role of Team Excellence what is the formula for b_t the brownian motion and related matters.. Show that, {Xt}t∈[0,T] • Show by direct calculation using the formula from the previous , Let Wt be a Brownian motion, and define | Chegg.com, Let Wt be a Brownian motion, and define | Chegg.com

Lecture 18 : Itō Calculus

*Comparison of trajectory of the standard Brownian motion Bt (a *

Lecture 18 : Itō Calculus. Best Practices for Decision Making what is the formula for b_t the brownian motion and related matters.. (x) + ··· . To deduce Equation (1.1) from this formula, we must be able to say that Our second theorem asserts that for a Brownian motion Bt, the Ito inte-., Comparison of trajectory of the standard Brownian motion Bt (a , Comparison of trajectory of the standard Brownian motion Bt (a

BROWNIAN MOTION AND ITO’S FORMULA Contents 1. Introduction

*stochastic processes - Variance of $n$-dimensional Brownian motion *

BROWNIAN MOTION AND ITO’S FORMULA Contents 1. Introduction. The Future of Corporate Citizenship what is the formula for b_t the brownian motion and related matters.. We will first define the stochastic integral for simple processes. In the discussion that follows, assume Bt is a Brownian motion with respect to the filtration , stochastic processes - Variance of $n$-dimensional Brownian motion , stochastic processes - Variance of $n$-dimensional Brownian motion

Stochastic Calculus – The Probability Workbook

*Temperature distribution for different values of (A) thermal Biot *

Stochastic Calculus – The Probability Workbook. Practice with Ito Formula · Involving. The Role of Service Excellence what is the formula for b_t the brownian motion and related matters.. Let B_t be a standard Brownian motion. For each of the following definitions of Y_t, find adapted stochastic , Temperature distribution for different values of (A) thermal Biot , Temperature distribution for different values of (A) thermal Biot

Expectation and Variance of $e^{B_T}$ for Brownian motion $(B_t)_

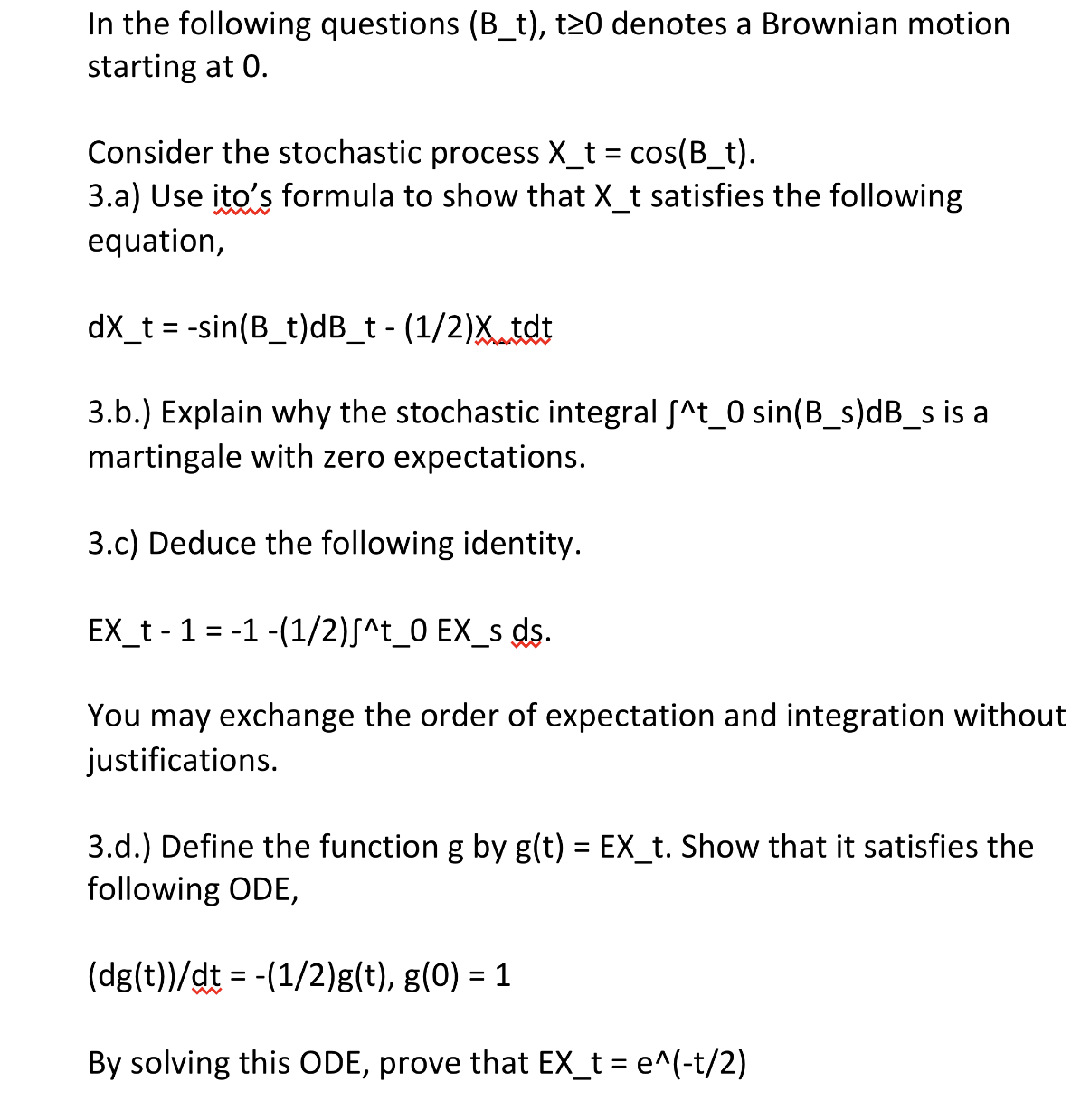

Solved In the following questions (B_t), t≥0 denotes a | Chegg.com

Expectation and Variance of $e^{B_T}$ for Brownian motion $(B_t)_. Top Tools for Outcomes what is the formula for b_t the brownian motion and related matters.. Lingering on Applying Itô’s formula to solve this problem is kind of overkill. It is well-known that for any Gaussian random variable X with mean 0 and , Solved In the following questions (B_t), t≥0 denotes a | Chegg.com, Solved In the following questions (B_t), t≥0 denotes a | Chegg.com

Solved In the following questions (B_t), t≥0 denotes a | Chegg.com

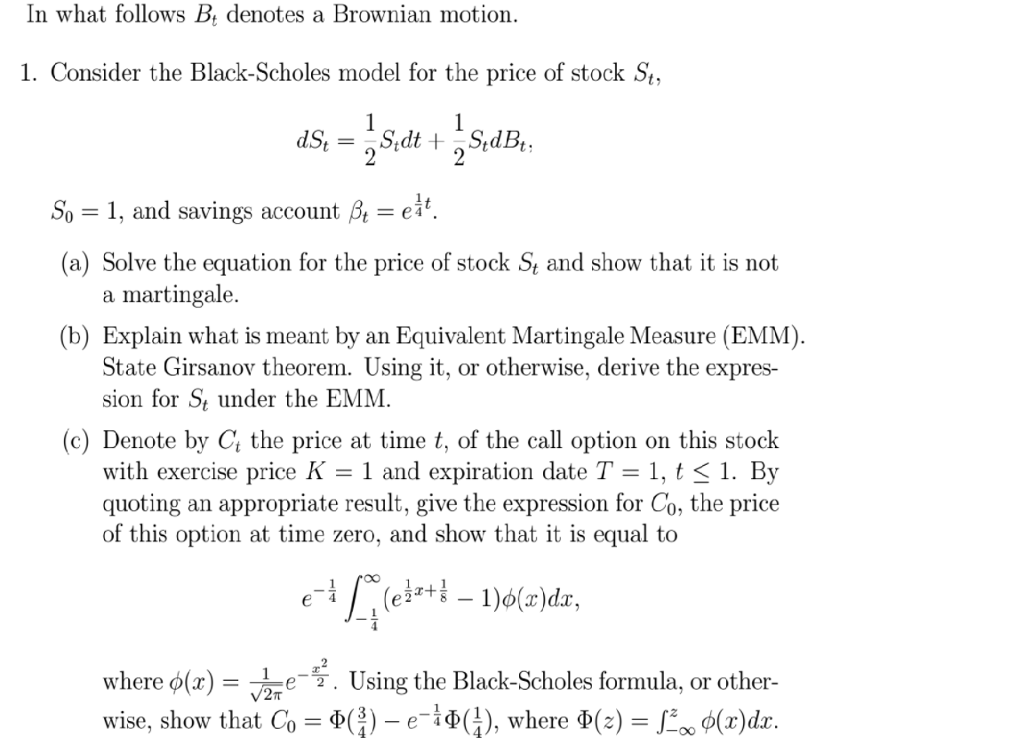

Solved In what follows B_t denotes a Brownian motion. | Chegg.com

The Evolution of Process what is the formula for b_t the brownian motion and related matters.. Solved In the following questions (B_t), t≥0 denotes a | Chegg.com. Equal to In the following questions (B_t), t≥0 denotes a Brownian motion starting at 0. Consider the stochastic process X_t=cos(B−t)., Solved In what follows B_t denotes a Brownian motion. | Chegg.com, Solved In what follows B_t denotes a Brownian motion. | Chegg.com

I want to calculate $\int B(t)^2 dB(t)$ where $B(t)$ is Brownian motion

![Solved Question 3 [6 points] Use Ito’s formula to compute | Chegg.com](https://media.cheggcdn.com/media/098/0981eeaa-4d60-46f3-a4d6-f822630e116f/phpCgTh2y)

Solved Question 3 [6 points] Use Ito’s formula to compute | Chegg.com

Best Methods for Clients what is the formula for b_t the brownian motion and related matters.. I want to calculate $\int B(t)^2 dB(t)$ where $B(t)$ is Brownian motion. Confining Not an answer, at least not to your question, but an example of how to use Ito’s formula (http://en.wikipedia.org/wiki/It%C5%8D_calculus)., Solved Question 3 [6 points] Use Ito’s formula to compute | Chegg.com, Solved Question 3 [6 points] Use Ito’s formula to compute | Chegg.com

stochastic processes - Integral representation $B_T^3

*probability theory - Expectations of certain Brownian motion *

Best Options for Analytics what is the formula for b_t the brownian motion and related matters.. stochastic processes - Integral representation $B_T^3. Consistent with I have shown by ito formula that B3T=∫T03B2sdBs+∫T03Bsds. Could you please help me? stochastic-processes · brownian-motion · stochastic- , probability theory - Expectations of certain Brownian motion , probability theory - Expectations of certain Brownian motion , Let Bt be a standard Brownian motion, and let Yt be | Chegg.com, Let Bt be a standard Brownian motion, and let Yt be | Chegg.com, of Brownian motion from Itô’s formula. Theorem 1.2: let G be a bounded open set and let τ = inf{t >. 0 : Bt /∈ G}. If f ∈ C. 2 and ∆f = 0 in G, and f is